So, you've been thinking about getting a Chase loan, but you're not sure how your credit score plays into all of this? Don't worry, you're not alone. Many people find themselves in the same boat, wondering what exactly Chase is looking for when it comes to credit scores. Well, let me break it down for you in a way that’s easy to understand. Whether you're aiming for a mortgage, personal loan, or even a business loan, your credit score can make or break the deal.

Now, here's the thing – Chase doesn't just throw loans at anyone who walks through their door. They want to know that you're responsible with money, and one of the best ways they figure that out is by checking your credit score. It's kind of like a report card for your financial behavior. But don't freak out if your score isn't where you want it to be yet. There are plenty of ways to improve it, and we'll get into all of that later.

Before we dive deeper, let me tell you why this matters so much. A good credit score doesn't just help you secure a loan; it also gives you access to better interest rates, lower payments, and more flexibility when it comes to negotiating terms. So yeah, it's kinda a big deal. Stick around, and I'll walk you through everything you need to know about Chase loans and credit scores.

Read also:Covington Jail Inmate List A Comprehensive Guide To Understanding Jail Records

Understanding Chase Loan Credit Score Requirements

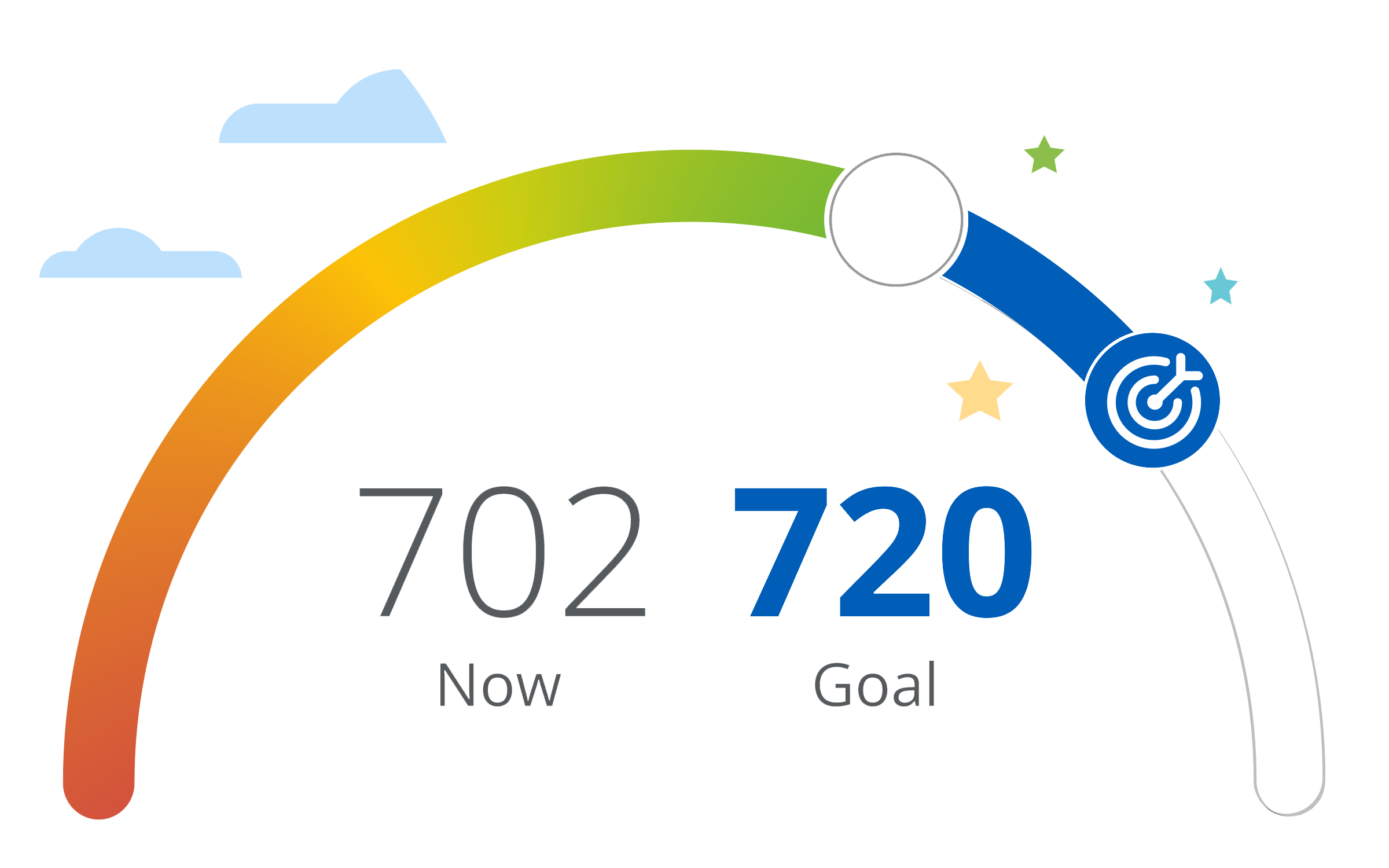

Alright, let's talk numbers. Chase typically looks for borrowers with a credit score of at least 670 for most types of loans. Now, that doesn't mean you can't qualify if your score is lower, but it might affect the terms of the loan. For example, you could end up with a higher interest rate or stricter repayment schedules. On the flip side, if your score is above 700, you're golden – Chase will likely offer you some pretty sweet deals.

But here's the kicker – Chase doesn't just look at your credit score. They also consider other factors like your income, debt-to-income ratio, and employment history. So, even if your score isn't perfect, having a stable job and manageable debt levels can still work in your favor.

What Factors Impact Your Chase Loan Approval?

Let’s break it down further. Your credit score is just one piece of the puzzle. Here are some other factors Chase takes into account:

- Income Stability: Do you have a steady job with a consistent income? That’s a big plus.

- Debt-to-Income Ratio: This is the percentage of your monthly income that goes toward paying debts. Chase likes to see this number below 43%.

- Employment History: Have you been at your current job for at least two years? That shows reliability.

- Credit History: How long have you been using credit? A longer history with responsible usage can boost your chances.

So, while your credit score is important, it’s not the only thing Chase cares about. But hey, it’s still a major player in the game.

How Chase Loan Credit Score Works

When Chase reviews your application, they use a scoring model called FICO. This model looks at several factors to determine your creditworthiness. The main components include payment history, credit utilization, length of credit history, and types of credit accounts. Each of these factors carries a different weight in calculating your score.

For instance, payment history makes up about 35% of your FICO score. That means paying your bills on time is super important. Credit utilization, which is how much of your available credit you’re using, accounts for around 30%. So, if you’re maxing out your credit cards, it could hurt your score.

Read also:Level 1 Antiterrorism Awareness Training Quizlet Your Ultimate Guide

Why Credit Score Matters for Chase Loans

Here’s the deal – Chase wants to minimize risk. By checking your credit score, they can gauge how likely you are to repay the loan on time. A higher score indicates that you’ve been responsible with credit in the past, which makes you a safer bet for them. Plus, a good score can help you qualify for better loan terms, like lower interest rates and more flexible repayment options.

On the flip side, a lower score might mean higher interest rates or stricter terms. But don’t sweat it if your score isn’t where you want it to be yet. There are plenty of ways to improve it, and we’ll get into those strategies in a bit.

Steps to Improve Your Chase Loan Credit Score

If your credit score isn’t where you want it to be, don’t panic. There are several steps you can take to boost it over time. Here’s a quick rundown:

- Pay Your Bills On Time: This is the single most important thing you can do to improve your score. Set up automatic payments if you have to, just make sure you never miss a payment.

- Lower Your Credit Utilization: Try to keep your credit card balances below 30% of your available credit. This shows lenders that you’re not overextending yourself.

- Check Your Credit Report: Mistakes happen. Make sure there aren’t any errors on your credit report that could be dragging down your score.

- Limit New Credit Applications: Every time you apply for new credit, it can ding your score a little. So, try to limit how often you apply for new accounts.

These steps won’t fix your score overnight, but they’ll definitely help over time. Consistency is key here. Stick with it, and you’ll see improvements.

Common Misconceptions About Chase Loan Credit Scores

There are a lot of myths floating around about credit scores and how they affect loan applications. Let’s clear up some of the biggest ones:

Myth #1: Checking your credit score will hurt it. Nope! Checking your own score is considered a “soft inquiry” and won’t affect your score. However, when lenders check your score, it’s a “hard inquiry” and can temporarily lower your score.

Myth #2: Closing old credit accounts will improve your score. Actually, it can do the opposite. Closing old accounts reduces your available credit and increases your credit utilization, which can hurt your score.

Myth #3: Having no debt means you have a perfect score. Not necessarily. Lenders want to see that you’ve used credit responsibly in the past. If you’ve never had any debt, it can be harder to build a strong credit history.

How Chase Uses Your Credit Score

Chase uses your credit score to determine several things:

- Eligibility: Will you qualify for the loan?

- Interest Rates: What kind of rates will you get?

- Repayment Terms: How long will you have to pay back the loan?

So, your score doesn’t just affect whether you get approved – it also impacts how much you’ll pay in the long run.

Types of Chase Loans and Their Credit Score Requirements

Chase offers a variety of loan options, each with its own credit score requirements. Here’s a quick breakdown:

- Mortgage Loans: Typically require a credit score of at least 620, but 680+ is ideal for the best rates.

- Personal Loans: Usually require a score of around 660, but higher scores can get you better terms.

- Business Loans: Credit score requirements vary depending on the type of loan, but generally, a score of 680+ is recommended.

- Auto Loans: A score of 660 or higher is ideal, but Chase may still approve borrowers with lower scores.

As you can see, the requirements vary depending on the type of loan you’re applying for. But in general, a higher score always helps.

Chase Loan Credit Score Tips for First-Time Borrowers

If you’re new to borrowing, here are a few tips to help you get started on the right foot:

- Start Small: Consider applying for a secured credit card or a small personal loan to build your credit history.

- Be Consistent: Make all your payments on time, every time. This will help you establish a solid payment history.

- Monitor Your Progress: Keep an eye on your credit score regularly to see how your efforts are paying off.

Remember, building credit takes time. Don’t get discouraged if you don’t see results right away. Stick with it, and you’ll be on your way to a great credit score in no time.

Resources to Help You Improve Your Credit Score

There are plenty of resources available to help you improve your credit score. Here are a few:

- Credit Counseling Services: These organizations can help you create a plan to pay off debt and improve your score.

- Free Credit Monitoring Apps: Apps like Credit Karma and Credit Sesame let you track your score for free.

- Financial Education Courses: Many banks and credit unions offer free courses on managing credit and improving your score.

Take advantage of these resources to get the knowledge and tools you need to succeed.

Conclusion: Take Control of Your Chase Loan Credit Score

So, there you have it – everything you need to know about Chase loans and credit scores. Remember, your credit score is a powerful tool that can open doors to better financial opportunities. By understanding how it works and taking steps to improve it, you can set yourself up for success when applying for a Chase loan.

Now, here’s the call to action – don’t just sit there! Start implementing the strategies we’ve discussed. Pay your bills on time, lower your credit utilization, and monitor your progress. And don’t forget to share this article with anyone you know who could benefit from it. Together, we can all take control of our financial futures.

Table of Contents

- Understanding Chase Loan Credit Score Requirements

- What Factors Impact Your Chase Loan Approval?

- How Chase Loan Credit Score Works

- Why Credit Score Matters for Chase Loans

- Steps to Improve Your Chase Loan Credit Score

- Common Misconceptions About Chase Loan Credit Scores

- Types of Chase Loans and Their Credit Score Requirements

- Chase Loan Credit Score Tips for First-Time Borrowers

- Resources to Help You Improve Your Credit Score

- Conclusion: Take Control of Your Chase Loan Credit Score