Looking for a way to finance your home improvement projects without breaking the bank? The Home Depot card with no interest could be your golden ticket! Whether you're planning a kitchen remodel, upgrading your bathroom, or just doing some routine maintenance, this credit card offers an attractive proposition for savvy shoppers. Let's dive into how it works, its benefits, and how you can take full advantage of it.

When it comes to home improvement, costs can pile up faster than you think. That’s where the Home Depot card steps in to save the day. With special financing options that include no interest for a limited time, this card is designed to help you tackle those big-ticket projects without the added stress of immediate payments. But is it really as good as it sounds?

In this comprehensive guide, we’ll break down everything you need to know about the Home Depot card no interest offer. From eligibility requirements to tips on maximizing your savings, we’ve got you covered. So grab a coffee, sit back, and let’s explore how this card could transform the way you approach home improvement.

Read also:Keith Conan Richter Released The Untold Story You Wont Believe

Understanding Home Depot Card No Interest Offers

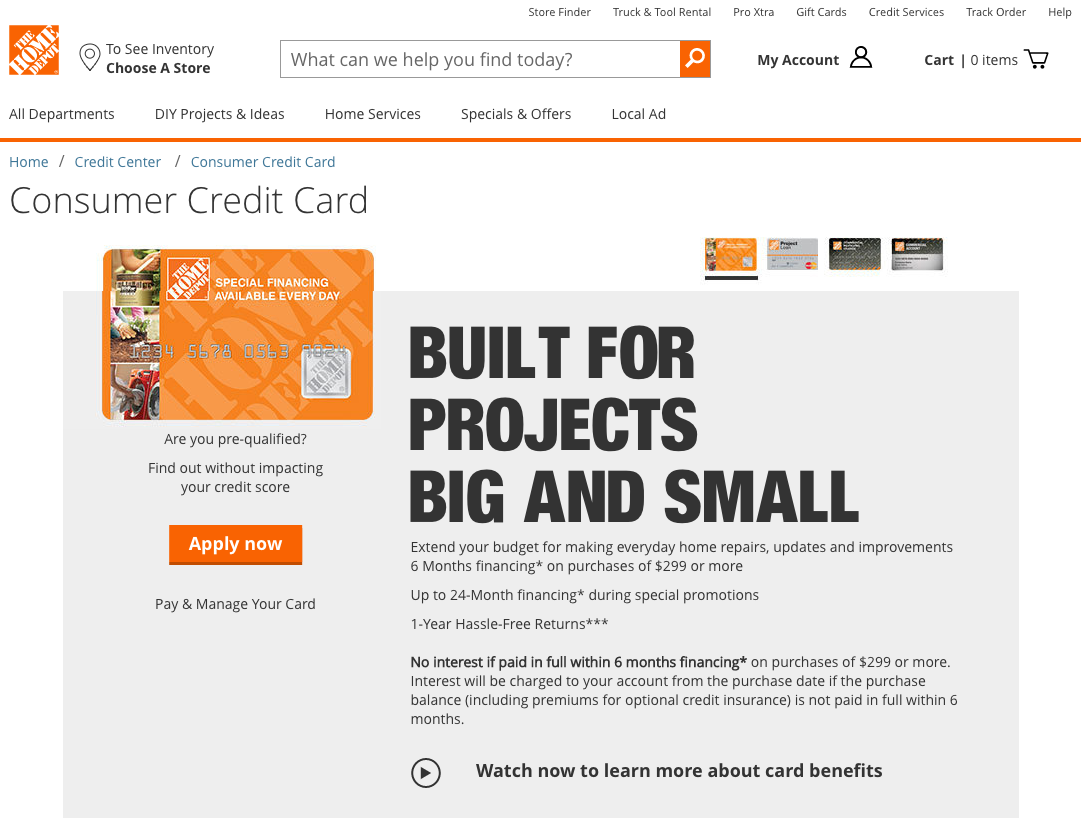

First things first, what exactly does "no interest" mean in the context of the Home Depot card? Simply put, it means that if you qualify for the special financing offer, you won’t have to pay any interest on your purchase for a specified period—usually ranging from 6 to 12 months, depending on the promotion. This is a game-changer for anyone looking to make substantial improvements to their home without the burden of interest charges.

How Does the No Interest Period Work?

Here’s the catch: while the no-interest period sounds fantastic, there are a few rules you need to follow to avoid unexpected charges. First, you must pay off the entire balance before the promotional period ends. If you don’t, you may end up paying interest retroactively on the original purchase amount. It’s like getting a free pass, but only if you stick to the terms.

For example, if you buy a new set of appliances worth $2,000 and the no-interest period lasts for 12 months, you’ll need to pay at least $166.67 per month to avoid interest charges. Miss that deadline, and the interest will kick in retroactively, which can add hundreds of dollars to your bill.

Benefits of the Home Depot Card No Interest Option

Now that we’ve covered the basics, let’s talk about why the Home Depot card no interest offer is such a big deal. Here are some of the top benefits:

- No Upfront Costs: You can start your project immediately without worrying about paying the full amount upfront.

- Flexibility: Use the card for a wide range of purchases, from appliances to landscaping equipment.

- Exclusive Discounts: Cardholders often enjoy exclusive discounts and promotions that aren’t available to regular customers.

- No Annual Fee: The Home Depot card doesn’t charge an annual fee, making it a cost-effective choice for occasional users.

Who Can Benefit Most from This Offer?

The Home Depot card no interest option is ideal for anyone planning a significant home improvement project. Whether you’re a homeowner looking to upgrade your living space or a renter wanting to personalize your apartment, this card can help you manage costs more effectively. It’s especially useful for large purchases like:

- Appliances (refrigerators, ovens, dishwashers)

- Plumbing fixtures (sinks, toilets, faucets)

- Lighting and electrical equipment

- Building materials (lumber, tiles, drywall)

Eligibility Requirements for the Home Depot Card

Before you jump in, it’s important to know whether you qualify for the Home Depot card no interest offer. While the card is open to most adults with a decent credit score, there are a few key factors to consider:

Read also:Who Is Terri Clarks Partner Unveiling The Life And Love Of A Country Music Icon

Credit Score Matters

Your credit score plays a huge role in determining your eligibility. Typically, you’ll need a credit score of at least 670 to qualify for the no-interest financing. However, higher scores may give you access to better terms and longer promotional periods. If your credit score isn’t where you want it to be, consider improving it before applying.

Income Verification

During the application process, you may be asked to provide details about your income. This helps the lender assess your ability to repay the balance within the no-interest period. Be honest and transparent to avoid any issues down the line.

How to Apply for the Home Depot Card No Interest Offer

Ready to apply? The process is straightforward and can be completed online or in-store. Here’s a quick step-by-step guide:

Step 1: Visit the Official Website

Head over to the official Home Depot credit card page to start your application. You’ll find all the necessary information about the card, including current promotions and terms.

Step 2: Fill Out the Application Form

The application form will ask for basic details like your name, address, Social Security number, and income. Make sure to double-check your entries for accuracy.

Step 3: Review the Terms and Conditions

Before submitting your application, take a moment to review the terms and conditions. This will help you understand exactly what you’re signing up for and ensure there are no surprises later.

Step 4: Wait for Approval

Once you’ve submitted your application, you’ll typically receive a decision within minutes. If approved, you’ll be able to start using your card right away.

Maximizing Your Savings with the Home Depot Card

Now that you’ve got your card, it’s time to make the most of it. Here are a few tips to help you save big:

Plan Your Purchases Carefully

Don’t just buy things on a whim. Make a list of everything you need for your project and stick to it. This will help you avoid overspending and ensure you can pay off your balance within the no-interest period.

Set Up Automatic Payments

One of the easiest ways to stay on top of your payments is to set up automatic transfers. This ensures you never miss a payment and helps you avoid interest charges.

Take Advantage of Rewards

Many Home Depot cardholders earn rewards points for their purchases. These points can be redeemed for discounts on future purchases, so it’s worth keeping track of them.

Potential Downsides to Consider

While the Home Depot card no interest offer has plenty of benefits, there are a few downsides to keep in mind:

High Interest Rates After the Promotional Period

If you fail to pay off your balance before the no-interest period ends, you’ll be hit with a high interest rate—often around 25% or more. This can quickly turn a great deal into a financial burden.

Impact on Credit Score

Applying for a new credit card can temporarily lower your credit score. Additionally, carrying a high balance relative to your credit limit can also have a negative impact. Use the card responsibly to minimize these effects.

Real-Life Success Stories

Don’t just take our word for it—here are a few real-life examples of how people have used the Home Depot card no interest offer to their advantage:

John’s Kitchen Remodel

John used his Home Depot card to finance a complete kitchen remodel. By paying off the balance within the 12-month no-interest period, he saved over $500 in interest charges. “It was like having an interest-free loan,” he said. “I’d definitely recommend it to anyone planning a similar project.”

Sarah’s Bathroom Upgrade

Sarah used her card to purchase new fixtures and tiles for her bathroom. “The no-interest period gave me the peace of mind to focus on the project without worrying about the financial side,” she explained. “And the exclusive discounts I got as a cardholder were an added bonus!”

FAQs About the Home Depot Card No Interest Offer

Can I Use the Card Outside of Home Depot?

No, the Home Depot card is designed specifically for use at Home Depot stores and online. However, it can still be used for a wide range of home improvement products and services.

What Happens if I Don’t Pay Off the Balance in Time?

If you don’t pay off the full balance before the no-interest period ends, you’ll be charged interest retroactively on the original purchase amount. This can significantly increase your total cost, so it’s crucial to stay on top of your payments.

Is the Home Depot Card Worth It if I Don’t Need the No Interest Offer?

Even if you don’t plan to use the no-interest financing, the Home Depot card can still be worth it for the rewards and discounts. Just be mindful of your spending habits to avoid accumulating debt.

Conclusion: Is the Home Depot Card Right for You?

By now, you should have a clear understanding of how the Home Depot card no interest offer works and whether it’s a good fit for your needs. While it offers significant benefits for those planning home improvement projects, it’s important to use it responsibly to avoid unnecessary debt.

Ready to take the next step? Apply for the Home Depot card today and start saving on your dream projects. And don’t forget to share your experiences in the comments below—we’d love to hear how the card has helped you!

Table of Contents

- Understanding Home Depot Card No Interest Offers

- Benefits of the Home Depot Card No Interest Option

- Eligibility Requirements for the Home Depot Card

- How to Apply for the Home Depot Card No Interest Offer

- Maximizing Your Savings with the Home Depot Card

- Potential Downsides to Consider

- Real-Life Success Stories

- FAQs About the Home Depot Card No Interest Offer

- Conclusion: Is the Home Depot Card Right for You?